目的変数や説明変数を対数変換すると、推定結果の解釈が変わる

| モデル | 係数の解釈 |

|---|---|

| 「が1単位増加すると、が単位増加する」 | |

| 「が1%増加すると、が単位増加する」 | |

| 「が1単位増加すると、が%増加する」 | |

| 「が1%増加すると、が%増加する」 |

次のようなデータを使って実際にモデルをあてはめつつ確認していく

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

import statsmodels.formula.api as smf

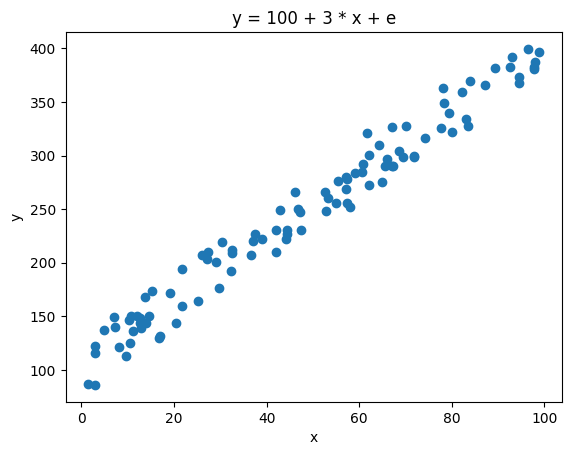

# 真のデータ生成過程

n = 100

np.random.seed(0)

x = np.random.uniform(1, 100, size=n)

x = np.sort(x)

e = np.random.normal(loc=0, scale=15, size=n)

beta0 = 100

beta1 = 3

y = beta0 + beta1 * x + e

df = pd.DataFrame({"y": y, "x": x})

plt.scatter(x, y)

plt.xlabel("x")

plt.ylabel("y")

plt.title(f"y = {beta0} + {beta1} * x + e")

plt.show()

Source

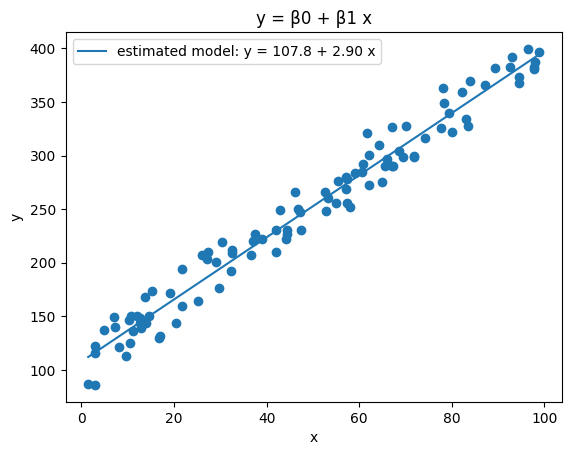

model = smf.ols('y ~ x', data=df).fit()

beta = model.params.to_list()

y_pred = model.predict(df[["x"]])

fig, ax = plt.subplots()

ax.scatter(x, y)

ax.set(xlabel="x", ylabel="y", title="y = β0 + β1 x")

ax.plot(x, y_pred, label=f"estimated model: y = {beta[0]:.1f} + {beta[1]:.2f} x")

ax.legend()

fig.show()

について

はテイラー近似から導出される。まずテイラー近似について述べる

とおくと、その次の微分は

となる。もしなら

となる。

これをでのテイラー展開(つまりマクローリン展開)

にあてはめると、

となる。これはが極めて小さな値()であればやといった値は非常に小さくなるため、となる。

よってとなる

数値計算的に確かめると、以下のようになる

import numpy as np

x = 0.01

print(f"log: {np.log(1 + x):.7f}")

print(f"approx 1: {x:.7f}")

print(f"approx 2: {x - (x**2 / 2):.7f}")

print(f"approx 3: {x - (x**2 / 2) + (x**3 / 3):.7f}")log: 0.0099503

approx 1: 0.0100000

approx 2: 0.0099500

approx 3: 0.0099503Source

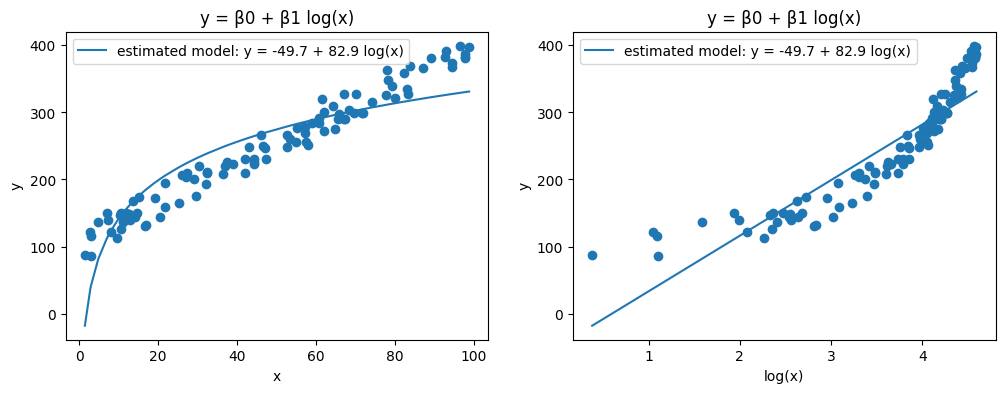

model = smf.ols('y ~ np.log(x)', data=df).fit()

beta = model.params.to_list()

y_pred = model.predict(df[["x"]])

fig, axes = plt.subplots(ncols=2, figsize=[12, 4])

axes[0].scatter(x, y)

axes[0].set(xlabel="x", ylabel="y", title="y = β0 + β1 log(x)")

axes[0].plot(x, y_pred, label=f"estimated model: y = {beta[0]:.1f} + {beta[1]:.3g} log(x)")

axes[0].legend()

axes[1].scatter(np.log(x), y)

axes[1].set(xlabel="log(x)", ylabel="y", title="y = β0 + β1 log(x)")

axes[1].plot(np.log(x), y_pred, label=f"estimated model: y = {beta[0]:.1f} + {beta[1]:.3g} log(x)")

axes[1].legend()

fig.show()

np.log(1.01)0.009950330853168092x0 = 50

y1 = beta[0] + beta[1] * np.log(x0)

y2 = beta[0] + beta[1] * np.log(x0 * 1.01)

print(f"xが1%増加したときのyの増分 = {y2 - y1:.3f}")xが1%増加したときのyの増分 = 0.825

の近似誤差が多少あるが、おおむね「が1%増加すると、が単位増加する」という関係になる。

について

とおくと、その次の微分は

となる。もしなら

となる。

これをでのテイラー展開(つまりマクローリン展開)

にあてはめると、

となる。

が極めて小さな値()であればやといった値は非常に小さくなるため、となる。

よってとなる

数値計算的に確かめると、以下のようになる

import numpy as np

x = 0.1

print(f"""

x : {x}

exp(x) - 1: {np.exp(x) - 1:.7f}

マクローリン近似

もとの値 exp(x) = {np.exp(x):.7f}

1次近似 1 + x = {1 + x:.7f}

2次近似 1 + x + (x^2 / 2!) = {1 + x + (x**2 / (1 * 2)):.7f}

""")x : 0.1

exp(x) - 1: 0.1051709

マクローリン近似

もとの値 exp(x) = 1.1051709

1次近似 1 + x = 1.1000000

2次近似 1 + x + (x^2 / 2!) = 1.1050000Source

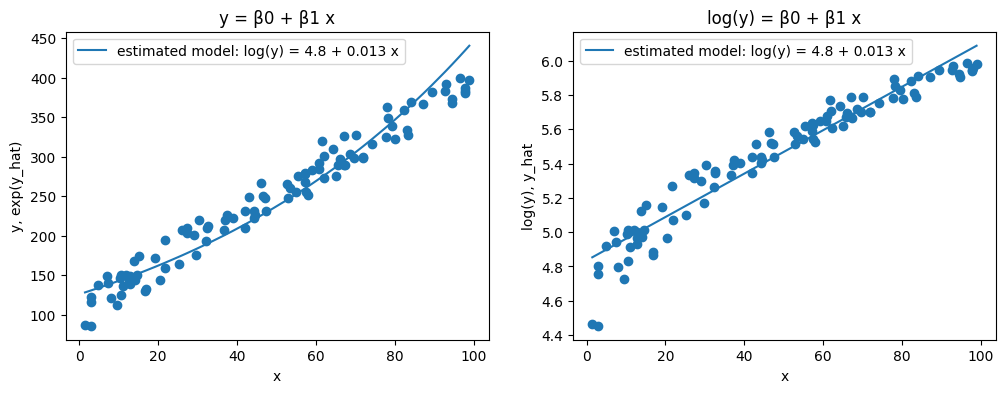

model = smf.ols('np.log(y) ~ x', data=df).fit()

beta = model.params.to_list()

y_pred = model.predict(df[["x"]])

fig, axes = plt.subplots(ncols=2, figsize=[12, 4])

axes[0].scatter(x, y)

axes[0].set(xlabel="x", ylabel="y, exp(y_hat)", title="y = β0 + β1 x")

axes[0].plot(x, np.exp(y_pred), label=f"estimated model: log(y) = {beta[0]:.1f} + {beta[1]:.2g} x")

axes[0].legend()

axes[1].scatter(x, np.log(y))

axes[1].set(xlabel="x", ylabel="log(y), y_hat", title="log(y) = β0 + β1 x")

axes[1].plot(x, y_pred, label=f"estimated model: log(y) = {beta[0]:.1f} + {beta[1]:.2g} x")

axes[1].legend()

fig.show()

x0 = 50

y1 = beta[0] + beta[1] * x0

y2 = beta[0] + beta[1] * (x0 + 1)

print(f"xが1単位増加したときのyの増分 = {y2 - y1:.3f}")xが1単位増加したときのyの増分 = 0.013

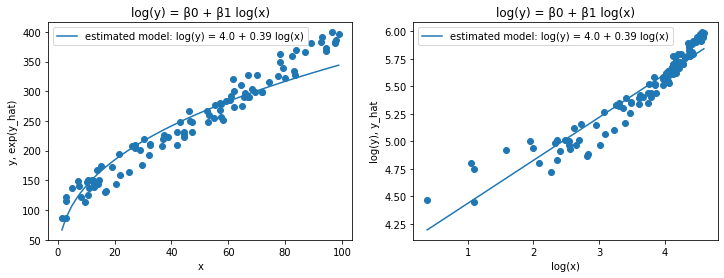

(4) ¶

「が1%増加すると、が%増加する」

Source

model = smf.ols('np.log(y) ~ np.log(x)', data=df).fit()

beta = model.params.to_list()

y_pred = model.predict(df[["x"]])

fig, axes = plt.subplots(ncols=2, figsize=[12, 4])

axes[0].scatter(x, y)

axes[0].set(xlabel="x", ylabel="y, exp(y_hat)", title="log(y) = β0 + β1 log(x)")

axes[0].plot(x, np.exp(y_pred), label=f"estimated model: log(y) = {beta[0]:.1f} + {beta[1]:.2g} log(x)")

axes[0].legend()

axes[1].scatter(np.log(x), np.log(y))

axes[1].set(xlabel="log(x)", ylabel="log(y), y_hat", title="log(y) = β0 + β1 log(x)")

axes[1].plot(np.log(x), y_pred, label=f"estimated model: log(y) = {beta[0]:.1f} + {beta[1]:.2g} log(x)")

axes[1].legend()

fig.show()

x0 = 50

y1 = beta[0] + beta[1] * np.log(x0)

y2 = beta[0] + beta[1] * np.log(x0 + 1)

print(f"xが1%増加したときのyの増分 = {y2 - y1:.3f}")xが1%増加したときのyの増分 = 0.008

y1 = model.predict(pd.DataFrame([{"x": x0}])).to_numpy()[0]

y2 = model.predict(pd.DataFrame([{"x": x0 + 1}])).to_numpy()[0]

print(f"xが1単位増加したときのyの増分 = {y2 - y1:.3f}")xが1単位増加したときのyの増分 = 0.008

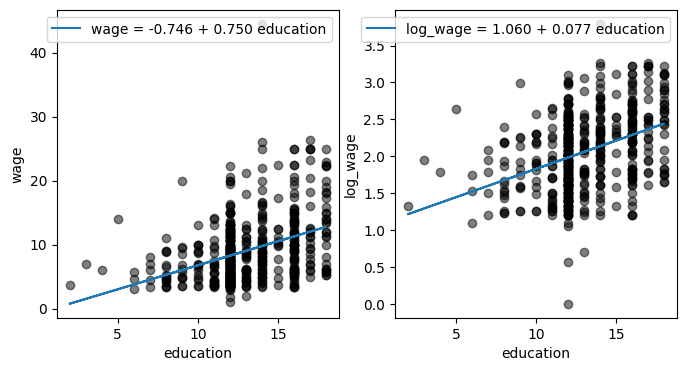

別データ例:賃金データ¶

RのAERパッケージに含まれるCPS1985という1985年の賃金のデータを例に取る。教育年数が1年ふえるごとに賃金は何%増えるのだろうか。

Source

import statsmodels.api as sm

cps = sm.datasets.get_rdataset("CPS1985", "AER").data.assign(log_wage = np.log(cps["wage"]))

fig, axes = plt.subplots(ncols=2, figsize=[8, 4])

reg = smf.ols('wage ~ education', data=cps).fit()

axes[0].scatter(cps["education"], cps["wage"], color="black", alpha=0.5

)axes[0].set(xlabel="education", ylabel="wage")

axes[0].plot(cps["education"], reg.predict(cps),

label=f"wage = {reg.params['Intercept']:.3f} + {reg.params['education']:.3f} education")

axes[0].legend()

reg = smf.ols('log_wage ~ education', data=cps).fit()

axes[1].scatter(cps["education"], cps["log_wage"], color="black", alpha=0.5)

axes[1].set(xlabel="education", ylabel="log_wage")

axes[1].plot(cps["education"], reg.predict(cps),

label=f"log_wage = {reg.params['Intercept']:.3f} + {reg.params['education']:.3f} education")

axes[1].legend()

モデルに投入するeducationの値が1上がるごとに、概ね0.079 = 7.9%程度上がる

reg = smf.ols('log_wage ~ education', data=cps).fit()

test = pd.DataFrame({"education": range(21)})

test["log_wage_pred"] = reg.predict(test) # 予測値を入れる

test["wage_pred"] = np.exp(test["log_wage_pred"])

test["wage_pred_diff"] = test["wage_pred"].diff()

test["wage_pred_change"] = test["wage_pred"].pct_change()

test["log_wage_pred_change"] = test["log_wage_pred"].pct_change()

test.head(10)Loading...

最近は逆双曲線変換をするらしい¶

長所:

対数と同様に振る舞う:被説明変数と説明変数両方にarsinh()している場合推定した回帰係数が弾力性になる(xとyが10以上などある程度大きい値のとき)

値がゼロの観測値を維持する:

値が負の観測値も維持する(があるため)

短所:

推定した係数が弾力性になるにはxとyが10以上などある程度大きい値のときのみ → 零や負の値を使えるという利点があまり活きない