Conformal Prediction (CP) は予測区間(prediction intervals)を算出するためのフレームワーク。

予測の残差から予測の幅を算出する。

DMLのcross-fittingのように、train setでは残差の予測モデルをfitせず、分けておいたcalibration setで残差の学習を行う。

前提¶

問題設定¶

個の訓練サンプルがあるとし、予測対象のサンプルもあるとする。 両方のデータは 交換可能(exchangeable) であると仮定する(例えばi.i.d.であるとする)。

が含まれると思われる marginal distribution-free prediction interval を構築したい。

exchangeability¶

サンプルが任意の同時分布から得られたものであり、サンプルの順列を変えても変わらないこと。i.i.d.よりは弱い仮定。

例えばサンプルが3つあるとして、 と は同じ同時分布を持つということ(Exchangeable random variables - Wikipedia)。

Conformal Regression¶

まず、訓練データを2つに分割する

training set:

calibration set:

任意の回帰アルゴリズムを用いて、回帰モデルを訓練する

calibration setで残差の絶対値を計算する

所与の水準のもとで、絶対残差の経験分布の分位点を計算する

新しく与えられた点での予測区間は

info - Unknown Directive

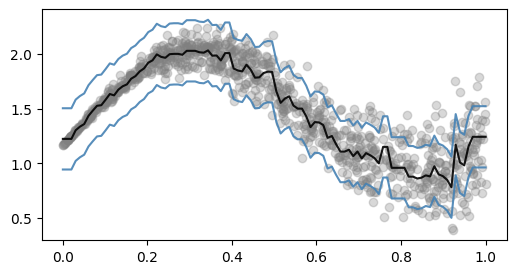

info - Unknown DirectiveAdaptiveではないConformal Predictionはどのデータ点$X$においても同じQuantile(区間の幅が固定)

Source

# generate data

import numpy as np

import matplotlib.pyplot as plt

n = 1000

np.random.seed(0)

x = np.random.uniform(low=0, high=1, size=n)

y = x**3 + 2 * np.exp(-6 * (x - 0.3)**2)

y = y + np.random.normal(loc=0, scale=x * 0.3, size=n)

from sklearn.model_selection import train_test_split

X = x.reshape(-1, 1)

X_train, X_cal, y_train, y_cal = train_test_split(X, y, test_size=0.33, random_state=42)

# calculate residual

from lightgbm import LGBMRegressor

model = LGBMRegressor(verbose=-1)

model.fit(X_train, y_train)

abs_residuals = np.abs(y_cal - model.predict(X_cal))

# aclculate quantile

quantile = np.quantile(abs_residuals, q=0.9)

# plot

x_range = np.linspace(x.min(), x.max(), 100)

y_pred = model.predict(x_range.reshape(-1, 1))

fig, ax = plt.subplots(figsize=[6, 3])

ax.scatter(x, y, alpha=0.3, color="gray")

ax.plot(x_range, y_pred, alpha=0.9, color="black")

ax.plot(x_range, y_pred + quantile, alpha=0.9, color="steelblue")

ax.plot(x_range, y_pred - quantile, alpha=0.9, color="steelblue")

fig.show()

Adaptive Conformal Prediction¶

区間の幅を可変にしたものの総称?

Conformalized quantile regression¶

locally adaptive