定常過程への変換¶

分析しやすいデータ:定常過程¶

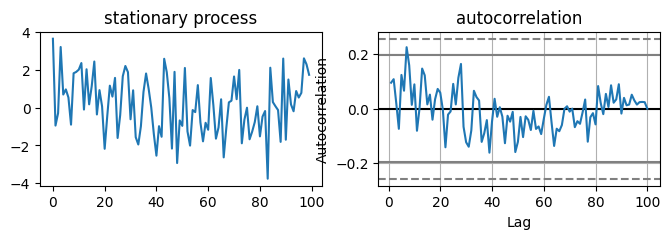

定常過程の場合、期待値や自己共分散が時間を通じて一定なので、例えば「1月の平均気温」は1月の各観測値の平均をとれば求められる。

ARIMAモデルは定常過程との相性がよいため、モデルを使った分析もしやすい。

Source

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

n = 100

np.random.seed(0)

mu = np.random.normal(size=n)

noise = np.random.normal(size=n)

y = mu + noise

fig, axes = plt.subplots(figsize=[8,2], ncols=2)

axes[0].plot(range(n), y)

axes[0].set(title="stationary process")

pd.plotting.autocorrelation_plot(y, ax=axes[1])

_ = axes[1].set(title="autocorrelation")