ベクトル自己回帰(VAR)モデル#

VARはARモデルの拡張版であり、VAR(\(p\))モデルは\(y_t\)を定数と自身の\(p\)次のラグ(\(p\)期の過去の値)に回帰したモデル。

モデル#

変数が\(n\)次元、ラグの次数が\(p\)だとする。(例えば時点\(t\)の観測値は \(y_{1,t}, y_{2,t}, \dots, y_{n,t}\) となる。)

VAR(\(p\)) では、各変数 \(y_{i,t}\) は、すべての変数の過去 \(p\) 期分の線形結合で表される。

\(\phi_{ij}^{(k)}\):変数 \(j\) の \(k\) 期前」が「変数 \(i\) の現在」に与える影響

\(\varepsilon_{i,t}\):変数 \(i\) に対応する誤差項

もう少しベクトルや行列を使って表すと、

\(\mathbf{c}\in\mathbb{R}^{n\times 1}\)

\(\boldsymbol{\Phi}_k \in\mathbb{R}^{n\times n}\)

ここで \(\rho=\operatorname{Corr}\left(\varepsilon_{1 t}, \varepsilon_{2 t}\right)\)

状態ベクトル \(\mathbf{y}_t \in \mathbb{R}^n\) 、 ラグ \(k\) の係数行列 \(\boldsymbol{Phi}_k \in \mathbb{R}^{n \times n}\)、 誤差ベクトル \(\boldsymbol{\varepsilon}_t\) をそれぞれ

とおくと、VAR(\(p\)) は次のように表現できる。

※切片を含めた表現もされる

パラメータ推定#

VARは一見複雑だが、本質的には各変数を同じ説明変数で回帰しているだけ(多変量回帰)である。例えばVAR(1) は \(\mathbf{y}_t = \mathbf{\Phi}_1 \mathbf{y}_{t-1} + \boldsymbol{\varepsilon}_t\) 。

サンプルサイズを \(T\) とする(初期 \(p\) 個は捨てる)。

目的変数行列を\(\mathbf{Y}\)、説明変数行列を\(\mathbf{Z}\)、係数行列をまとめたものを\(\mathbf{B}\)とおく。

VARはOLSで推定可能

実装#

Vector Autoregressions tsa.vector_ar - statsmodels 0.14.6

import numpy as np

import pandas

import statsmodels.api as sm

from statsmodels.tsa.api import VAR

mdata = sm.datasets.macrodata.load_pandas().data

# prepare the dates index

dates = mdata[['year', 'quarter']].astype(int).astype(str)

quarterly = dates["year"] + "Q" + dates["quarter"]

from statsmodels.tsa.base.datetools import dates_from_str

quarterly = dates_from_str(quarterly)

mdata = mdata[['realgdp', 'realcons']]

mdata.index = pandas.DatetimeIndex(quarterly)

data = np.log(mdata).diff().dropna()

# data

display(data.tail())

# make a VAR model

model = VAR(data)

results = model.fit(2)

results.summary()

| realgdp | realcons | |

|---|---|---|

| 2008-09-30 | -0.006781 | -0.008948 |

| 2008-12-31 | -0.013805 | -0.007843 |

| 2009-03-31 | -0.016612 | 0.001511 |

| 2009-06-30 | -0.001851 | -0.002196 |

| 2009-09-30 | 0.006862 | 0.007265 |

/home/runner/work/notes/notes/.venv/lib/python3.10/site-packages/statsmodels/tsa/base/tsa_model.py:473: ValueWarning: No frequency information was provided, so inferred frequency QE-DEC will be used.

self._init_dates(dates, freq)

Summary of Regression Results

==================================

Model: VAR

Method: OLS

Date: Sun, 21, Jun, 2026

Time: 23:33:23

--------------------------------------------------------------------

No. of Equations: 2.00000 BIC: -20.0648

Nobs: 200.000 HQIC: -20.1630

Log likelihood: 1465.40 FPE: 1.63813e-09

AIC: -20.2297 Det(Omega_mle): 1.55920e-09

--------------------------------------------------------------------

Results for equation realgdp

==============================================================================

coefficient std. error t-stat prob

------------------------------------------------------------------------------

const 0.001024 0.000971 1.055 0.291

L1.realgdp -0.096477 0.087307 -1.105 0.269

L1.realcons 0.571453 0.102953 5.551 0.000

L2.realgdp -0.038461 0.081226 -0.474 0.636

L2.realcons 0.352325 0.109914 3.205 0.001

==============================================================================

Results for equation realcons

==============================================================================

coefficient std. error t-stat prob

------------------------------------------------------------------------------

const 0.004668 0.000843 5.538 0.000

L1.realgdp 0.051847 0.075826 0.684 0.494

L1.realcons 0.194414 0.089414 2.174 0.030

L2.realgdp 0.013699 0.070545 0.194 0.846

L2.realcons 0.181398 0.095460 1.900 0.057

==============================================================================

Correlation matrix of residuals

realgdp realcons

realgdp 1.000000 0.603188

realcons 0.603188 1.000000

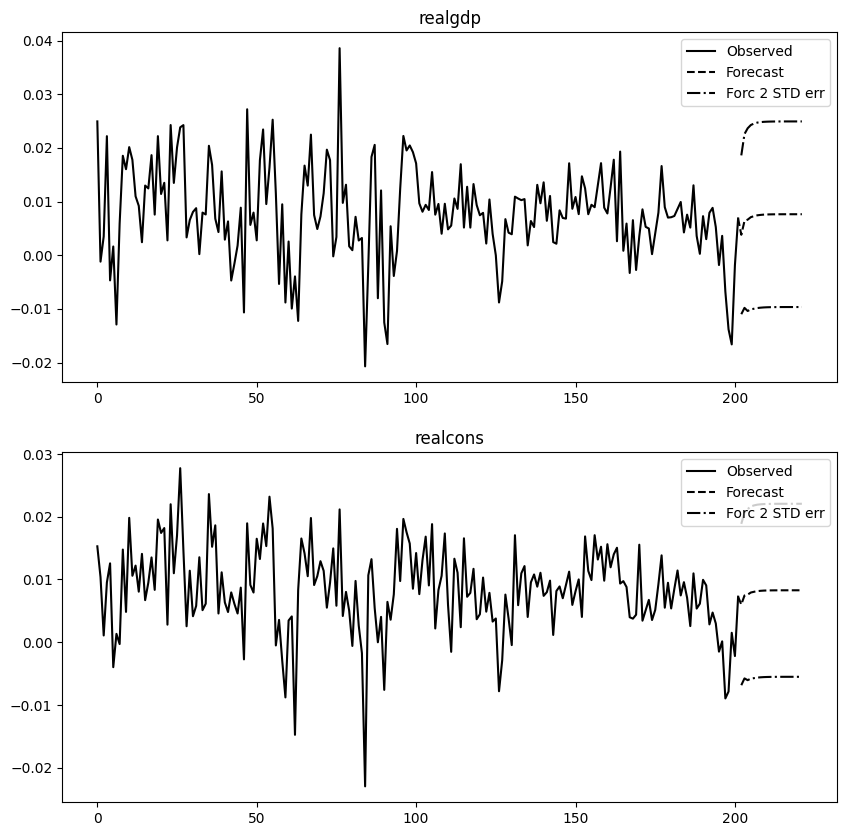

_ = results.plot_forecast(steps=20)